I am delighted Duncan Smith[1] responded positively to my request to write a Guest Briefing for Oxford House. The Briefing is a taster of his treatment of an important theme.

Christopher Hancock (Director)

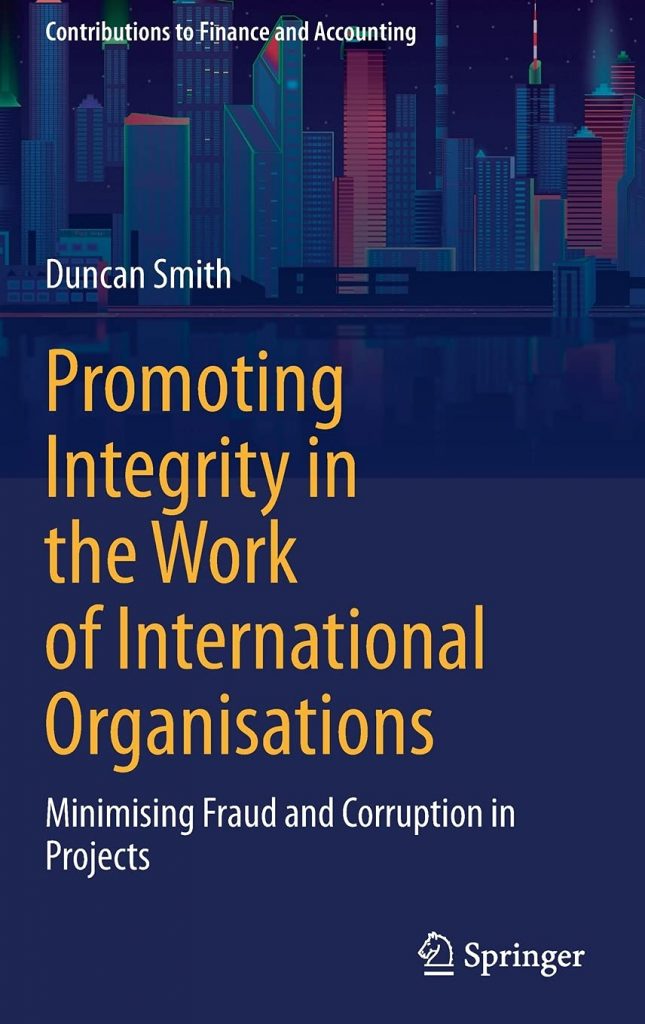

Frauds and tricksters are common in fiction. From the Wizard of Oz to The Talented Mr Ripley fictional characters have portrayed the alluring arts of deceit and corruption. What’s more, as Stephen May wrote a few years ago, ‘Fakers, phonies and frauds: tragically these can be some of the most dazzling, most beguiling – and most fun – people you can meet’ (The Guardian, 12 March 2014)! I am delighted to have this opportunity to introduce the book I wrote recently on the world some of these all-too-real characters inhabit. Hopefully, the book’s central focus will resonate with all who have struggled to manage or monitor international organizations (large and small) and the projects they fund around the world, or who have wondered (or worried) who or what can stop corruption spreading. My book is rather bluntly entitled Promoting Integrity in the Work of International Organisations – Minimizing Fraud and Corruption in Projects (Springer, 2021), and, as they say, ‘It aims to do what it says on the tin.’ Prior to my present position as Deputy Head of Investigations at the European Investment Bank (EIB), Luxembourg, I held a similar position at World Bank Investigations in Washington, DC. Before that I was a barrister in Gray’s Inn, London in the late 1980s and worked for the UK’s Department of Trade and Industry and the Serious Fraud Office. At the heart of all these jobs – as in my work as a member of the Secretariat of the Conference of International Investigators (2001-17) and when I prepared a number of papers for the Multilateral Development Banks (MDBs) whilst at the World Bank and EIB – were the fundamental issues of integrity and compliance. The book is an overview of the complex legal structures, risks and practical protocols associated with ensuring international organisations also can ‘do what they say on the tin’. The book is 200+ pages: it could have been a lot longer!

Books start for many reasons and often – rightly – never end. Promoting Integrity in the Work of International Organisations began by chance, or, more accurately, by accident. In 2018 I was knocked off my bike, broke my neck and sustained significant head injuries.[2] Recovery was long, slow and hard. As part of the recovery process, I started making notes on my work and practical experience as a lawyer specializing in fraud, corruption and compliance cases. A friend, who came to visit me at home (once I had been released from 12 weeks in hospital but undergoing another year of outpatient treatment and exercises), read my notes and encouraged me to consider turning them into a book. I finally did – after a lot more work! But the book and the work will never really end; that is, as long as human nature and modern institutions large and small are exposed to the challenges of good, ethical management and the invasive temptations to cut corners, misreport income and expenditure, cheat and bend rules and overlook backhanders. As I know all too well – not least from turning first-hand experience into policy and training – the issue isn’t just, ‘Do people know the rules’, but ‘Do they apply them’, and ‘What needs to be done to try to ensure that they do’ – and, let’s be clear, it’s not just for their sake, but for the sake of every system that is lubricated by integrity and snarled up by corruption. And, from my everyday experience, fraud and corruption are – counter-intuitively perhaps – profoundly self-destructive and can cause long term damage. As William Shakespeare wrote, ‘Corruption wins not more than honesty’ (Henry VIII, Ac. 3, Sc. 2.1.441).

To bring clarity, definition, and order to a large and complex area of international commercial law and practical governance, the book focusses on four key themes: i. the problems and risks of fraud and corruption (esp. Chapters. 3-6); ii. the activities taken by organisations to detect and prevent them (esp. Chapters 10-14); iii. the commercial safeguards that are, or should be, invoked (esp. Chapters 7-9); and iv. the results, outcomes and follow-up that again are, or should be, associated with fraud, corruption and compliance (esp. Chapter 15). But it is an ever-evolving picture. The case studies I cite will soon need to be changed or supplemented by others in the very near future. Crime – though sadly predictable – is remarkably creative.

The particular focus of my work (and book) in the last few years has been to promote integrity, and minimize fraud and corruption, in the work of international organisations. In particular, I have been involved in monitoring project finance sourced from MDBs, such as the European Investment Bank (EIB), the World Bank (WB), the Asian Development Bank (ADB), the Inter-American Development Bank (IADB), African Development Bank (ADB) and the European Bank for Reconstruction and Development (EBRD). It is not surprising that the misuse of funds by local recipients (and even careless distribution of charitable support by international donors) have attracted media attention and stirred public protests. Like cracked pipes and irregular water supplies, greed and inefficiency, bribery and waste, compromise the aims of funders/donors and responsibilities of beneficiaries. So, deterrence, prevention, detection and monitored reporting are increasingly becoming central to the financial transparency in projects financed by many international organisations. Funds must be seen to reach the intended recipient or cause, while operations, projects, and activities must be demonstrably free from fraud and corruption. This is no small task, as my book makes clear.

When I have had to speak on these issues at universities or professional gatherings, I have been acutely aware that listeners will come with their own set of expectations and awareness of malpractice. So, when I address the problems and risks of fraud and corruption, I have in mind the types of large-scale fraud some will be aware of (like Madoff, BCCI and Enron), which have often had a knock-on effect on projects and significant repercussions to the economy and taxpayer, and of high-profile projects and bodies that are associated with giving or receiving substantial amounts of money (such as the Global Fund to fight AIDS, Tuberculosis and Malaria, the United Nations’ Development Programme and UNICEF, and the World Food Program). In Chapter 14 of my book, I cite some ‘Notable Cases’ of fraud and corruption that are linked to settlements and MDB sanctions (e.g., Siemens, Alstom, Oxford University Press, Odebrecht and SNC Lavalin), which impacted the work of MDBs more generally. Other cases might have been cited, some of which affected domestic jurisdictions. The sad reality is that the work of MDBs, and other donor agencies as a whole, is compromised if good practice is not seen and trusted. The truism of a bad apple in a barrel definitely applies!

So, how can fraud, corruption, mismanagement and mistrust be avoided? It isn’t easy. Forces of every kind, from ambition to acquisitiveness and the sheer thrill of trying to outwit monitoring bodies, militate against good practice and due process. Hence, my book begins from two clear starting points. First, the original conception of an MDB-type, or large scale, project. The early stages of procurement, assessment of bids, the award of contracts and implementation of the project – be it civil works or provision of equipment (e.g., for a medical, educational, hydro-electric generation or infra-structure project) – are crucial. For all parties to be clear (preferably from the outset) about timelines, costs, accountability, responsibility, future management, and individual, community, commercial or government expectations, is vital. Whether it be the construction of a hospital, dam or railway, or the provision of textbooks or classrooms, clarity is absolutely key. The same applies to the second starting point; namely, agreed definitions of (what EIB technically calls) ‘Prohibited Conduct’, including everything from diverting funds to the benefit of officials, misrepresentations, bid-rigging, and money laundering for criminal activities, to the use of funds to finance terrorism. If you think these – and many other things – haven’t happened, think again! MDB and large-scale project funding is at risk precisely because it is large scale and deemed susceptible to less careful scrutiny. It may seem obvious, but if there isn’t agreement about due process, integrity and potential risk/s, projects can be doomed from the start. My book is a sustained, practical appeal to ensure this doesn’t happen.

When you drill down into these two starting points of ‘process’ and ‘risk’ other consequences and requirements emerge. Hence, my book looks in detail at the role compliance, business ethics, corporate governance, and a host of other safeguards that companies and funders can use as preventative measures against fraud, corruption and mismanagement; and I include in this the appointment of consultants and advisers to help funders monitor projects. It helps enormously if all parties understand the terms and conditions that are normally employed in a contract or finance agreement with an MDB. This includes, for example, the implementing agency’s use in procurement of the EIB’s ‘covenant of integrity’ and the World Bank’s ‘disclosure’ (in its standard bidding documents) of agent’s fees. So, no-one can turn round and say, ‘You didn’t tell us …’ or ‘We assumed that wasn’t important’. No, the exclusion of uncertainty is vital. There should be no room for confusion either over definitions of fraud or corruption, collusion or coercion (N.B. the guidelines on this in the International Finance Institutions’ Anti-Corruption Task Force’s Uniform Framework, 2006). Likewise, there should be clarity over accepted investigation procedures and sanctioning decisions that lead to ‘cross-debarment’ as per the agreement cited below between five of the major MDBs.[3] If it sounds intimidating, it probably should do, and the deterrent effect increases.

If clarity is vital in the work I do, so is candour. Hence, my book includes a short review of cyber-crime, data protection and money laundering (involving commercial banks such as Danske Bank, Standard Chartered, Swedbank and the Troika Laundromat) and the role of the Financial Action Task Force (FATF) in setting standards and promoting effective implementation of legal, regulatory and operational measures to combat money laundering, terrorist financing and related threats to the integrity of the international financial system. I also outline the various ways in which the organisations can, and should, act to detect ‘Prohibited Conduct’, through a process of investigating allegations, proactively red flagging risks or potential weaknesses in an implementing agency’s procedures and processes, and proposing strategies to mitigate such gaps going forward. Alongside this, a skeptical public and wary donor or investor large and small, can take comfort from the extensive investigation and prosecution work undertaken year-in-year-out by national criminal law enforcement agencies (such as the UK’s Serious Fraud Office and US Department of Justice) with the prosecutions, convictions and the so-called ‘Deferred Prosecution Agreement’ with Rolls Royce, Tesco and GSK that have resulted, and sundry ‘Unexplained Wealth Orders’. The reassuring fact is, MDBs and other major financers/donors are both accountable to and defenders of an increasingly tightly monitored space, where entities are both deterred and sanctioned, and legal instruments – such as the ‘Cross-Debarment Agreement’ (2010),[4] by which major MDBs enforce each other’s debarment of contractors/consultants for corruption, fraud, coercion and collusion – are invoked. What’s more, as my book indicates, there are many other organisations and sources of information for corporations and entities that are seeking assistance for the various kinds of risk they face; in particular, the OECD, B20 Collective Action Hub, Open Contracting Partnership, Transparency International, the Basel Institute on Governance, the International Anti- Corruption Academy (IACA), all of which exist to provide sound advice and practical guidance. And never underestimate the value of blockbuster films that deal with fraud and corruption: though they may inspire criminals, they can also help to raise awareness of the risks and countermeasures in place to counter corruption (N.B., I list some of these films in the Annex to my book).

Let me end with Shakespeare again, whose ambiguous character Angelo in Measure for Measure makes a strong appeal for law to be honoured: ‘We must not make a scarecrow of the law, setting it up to fear the birds of prey, and let it keep one shape till custom make it their perch and not their terror’ (Measure for Measure, Ac. 2, Sc. 1.1-4). There will always be rogues and villains in national and international life: the challenge we all face is not to allow them to make a mockery of the law, which in the end holds a society together in peace and security.

Duncan Smith (in collaboration with the Director)

[1] Duncan Smith is presently Deputy Head of Investigations at the European Investment Bank (EIB), Luxembourg.

[2] Proceeds from sales of the book will be remitted to the UK brain injury charity ‘Headway’ (cf. headway.org.uk).

[3] Cf. EBRD, African Development Bank, Asian Development Bank, World Bank and Inter-American Development Bank; EIB is not a signatory for legal reasons.

[4] This agreement was implemented over a period of time, viz. Asian Development Bank and EBRD (9 June 2010), World Bank (19 July 2010), Inter-American Development Bank (9 May 2011) and African Development Bank (11 July 2012).